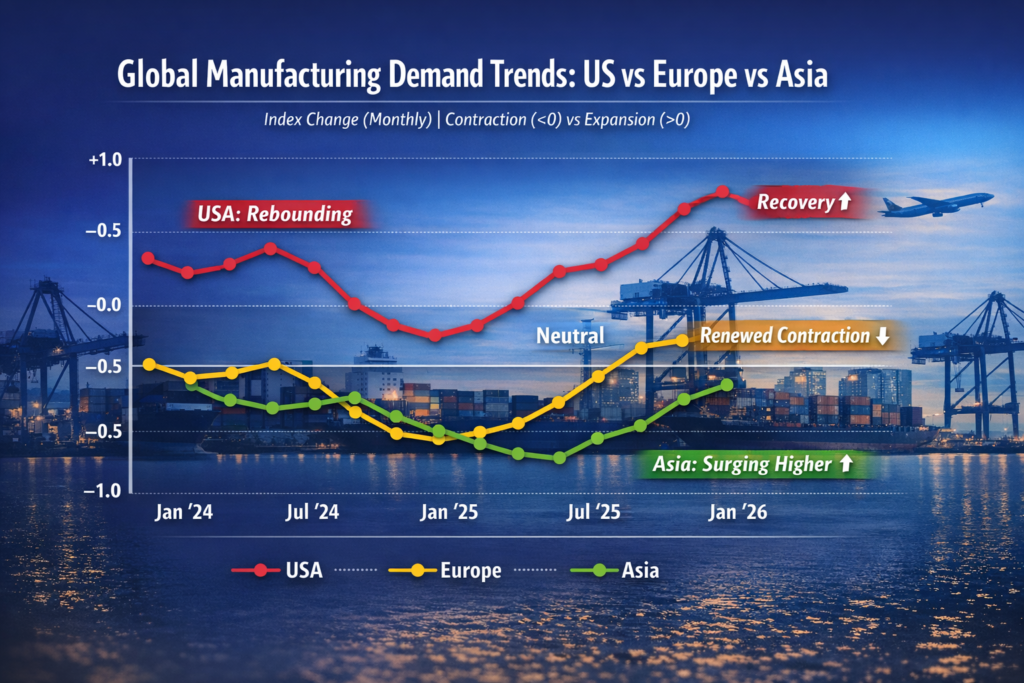

Global manufacturing demand surged to its strongest level in nearly four years in January 2026, signalling a renewed upswing in global trade and procurement activity. According to the GEP Global Supply Chain Volatility Index, compiled by S&P Global and GEP, purchasing activity for raw materials, components and commodities expanded at the fastest pace since May 2022.

The rebound was broad-based but regionally uneven — with Asia and the United States leading, while Europe remained subdued.

Country-Wise Demand & Import Trends: 2024–2025 Snapshot

To understand where this demand is coming from, it is important to look at recent import and apparel sourcing data.

🇺🇸 United States

The US remains the world’s largest apparel importer.

- 2024 US apparel imports: approx. US$ 82–85 billion

- 2025 (estimated): Flat to marginal growth after inventory correction in 2023

- Major sourcing countries: China, Vietnam, Bangladesh, India

In 2023, US imports declined sharply due to overstocking. However, 2024 saw stabilisation, and late 2025 data indicated gradual restocking — now reflected in January 2026’s stronger procurement index.

The January rebound suggests US brands are:

- Increasing raw material purchases

- Rebuilding core inventory

- Preparing for stronger seasonal pipelines

This is particularly relevant for Asian manufacturing hubs.

🇪🇺 European Union

The EU collectively imports over US$ 180–200 billion worth of apparel annually (intra + extra EU trade combined).

However:

- 2023–2024 saw weak consumer sentiment

- Germany and France reported slower discretionary spending

- Retail inventory adjustments extended into 2025

January 2026 data shows Europe still lagging, with spare supplier capacity and cautious restocking. This suggests EU demand recovery is slower than the US.

🇨🇳 China

China’s role is dual:

- Major exporter

- Massive domestic manufacturing consumer

China’s textile and raw material imports rose in late 2025 amid domestic industrial stimulus and export order stabilisation.

The January index indicates Chinese manufacturers increased procurement, signalling improved export visibility.

🇻🇳 Vietnam

Vietnam remains the second-largest apparel exporter to the US after China.

- 2024 apparel exports: approx. US$ 40+ billion

- US accounts for over 40% of exports

Vietnam benefited from supply chain diversification and continues to gain share in sportswear and performance categories.

🇮🇳 India

India’s textile and apparel exports stood around US$ 34–36 billion in 2024, with steady growth in yarn and fabric exports.

Rising material procurement in January suggests stronger downstream production orders.

Data Table Summary: Global Demand & Apparel Trade Snapshot

| Region / Country | 2024-25 Apparel Import / Export (Approx.) | Demand Trend (Late 2025 – Jan 2026) | Manufacturing Impact | Implication for Bangladesh |

| United States | US$ 82-85 bn apparel imports | Recovery & restocking | Higher procurement, tighter supplier capacity | Strong opportunity (US is 20-22% of BD exports) |

| European Union | US$ 180-200 bn apparel imports | Weak, cautious buying | Spare supplier capacity | Risk (EU >50% of BD exports) |

| China | Major exporter + raw material hub | Strong material procurement | Textile & component production up | Competition + upstream sourcing partner |

| Vietnam | US$ 40+ bn apparel exports | Benefiting from US demand | Capacity tightening | Direct competitor in US market |

| India | US$ 34-36 bn textile & apparel exports | Rising material demand | Yarn & fabric output rising | Competes in cotton-based segments |

| Bangladesh | US$ 47-48 bn apparel exports | Gradual improvement | Dependent on US rebound | Needs strategic positioning |

•Figures are based on recent trade trends and 2024–25 export performance estimates

Asia: The Manufacturing Engine of the Recovery

The January reading shows Asia’s supply chains operating at their busiest since late 2024. Increased purchasing activity in:

- China

- Japan

- South Korea

- India

- ASEAN economies

indicates that brands are placing upstream material orders — a leading indicator of future finished goods production.

This is significant for the global apparel value chain because material procurement typically precedes export shipments by 2–4 months.

US Demand: The Key Trigger

The US manufacturing rebound is one of the clearest signals in the January data. North America’s index moved back into expansion, showing:

- Higher procurement volumes

- Increased inventory building

- Supplier capacity tightening

This suggests US brands are regaining confidence after two years of cautious buying.

For apparel exporters, stronger US demand generally translates into higher order flow for:

- Basic knitwear

- Denim

- Casualwear

- Private label essentials

Europe: Still in Wait-and-Watch Mode

Europe’s index remained in contraction territory, indicating spare supplier capacity and limited restocking appetite.

For exporters heavily dependent on EU buyers, this means:

- Price negotiations remain tight

- Lead times may extend due to cautious scheduling

- Volume recovery may be gradual

Has Bangladesh Benefited from the Upswing?

Bangladesh exported approximately US$ 47–48 billion in apparel in FY2024–25, with:

- The US accounting for around 20–22%

- The EU accounting for over 50%

Given that:

- US demand is strengthening

- Europe remains weak

- Material shortages are below long-run averages

Bangladesh stands to gain primarily through US-focused buyers.

Positive Indicators for Bangladesh:

- Stable raw material supply environment

- Lower global labour bottlenecks

- US restocking cycle improving

Risks:

- Higher oil prices raising freight costs

- EU demand still fragile

- Increasing competition from Vietnam and India

If US procurement momentum continues through Q2 2026, Bangladesh could see improved order inflows — particularly in value-driven, high-volume segments.

What This Means for Global Apparel Trade in 2026

The January surge in global manufacturing demand signals:

✔ Stronger upstream raw material buying

✔ Asia-led production expansion

✔ US retail confidence returning

✔ Limited supply chain disruptions

However, a full global recovery depends on Europe stabilising consumption.

For Bangladesh and other Asian exporters, the next quarter will determine whether this rebound translates into sustained export growth or remains a short-term restocking cycle.

(Apparel Times BD Desk)

**Sources: GEP Global Supply Chain Volatility Index (January 2026), S&P Global PMI data, and latest official trade statistics from OTEXA, Eurostat, EPB and respective national authorities.**